The stock market is off to a volatile start to 2026. The Nasdaq-100 technology index was down by as much as 12% from its peak in March, only to recover all of its losses and hit a new record high in April. Investors have been trying to price in the potential economic impacts of the wild swings in oil prices, caused by the geopolitical conflict between the U.S. and Iran.

But Wall Street’s attention will soon be on the operating performance of some of America’s largest technology companies. On April 29, Microsoft (MSFT 0.56%) will release its financial results for its fiscal 2026 third quarter (ended March 31), which will include valuable updates on artificial intelligence (AI) products and services such as the Copilot virtual assistant, and the Azure cloud platform.

Microsoft stock is currently down 22% from its record high, but here’s why the April 29 report could be a very bullish catalyst.

Image source: Getty Images.

Copilot adoption will be front-and-center

AI chatbots are a dime a dozen right now, so it’s unlikely all of them will survive over the long term. However, Copilot has a distinct advantage, because it’s being deployed into Microsoft’s existing software products that collectively serve billions of users around the world already.

Copilot is available for free in the Windows operating system, the Bing search engine, and the Edge internet browser, but it can also be added to enterprise versions of the 365 productivity suite (which includes Word, Excel, Outlook, and more) for an additional subscription fee. This is a huge financial opportunity for Microsoft, because companies around the world already pay for over 400 million 365 licenses for their employees, and every one of them is a candidate for the Copilot upgrade.

But as of Dec. 31, businesses had only bought 15 million Copilot for 365 licenses, representing a modest penetration rate of just 3.7%. On the plus side, that figure was up 160% year over year, and some of the usage metrics suggest once businesses start using Copilot, they tend to introduce it to more of their employees over time.

Microsoft is likely to provide an update on Copilot adoption on April 29, and investors will probably want to see more triple-digit percentage growth given the relatively low base license number.

Today’s Change

(-0.56%) $-2.36

Current Price

$420.43

Key Data Points

Market Cap

$3.1T

Day’s Range

$417.12 – $423.13

52wk Range

$355.67 – $555.45

Volume

319K

Avg Vol

38M

Gross Margin

68.59%

Dividend Yield

0.82%

Azure was likely Microsoft’s growth engine (again) in Q3

Over the past four quarters, Microsoft spent $118 billion to build data centers that house thousands of specialized chips from Nvidia and other suppliers. It rents this infrastructure to businesses through its Azure cloud platform, and they use it to develop AI models and software for their own purposes.

Azure revenue grew at a blistering pace of at least 39% year over year in each of the first two quarters of fiscal 2026, making it Microsoft’s fastest-growing segment. Azure could be growing even faster, but Microsoft simply can’t build data centers quickly enough to meet demand. In fact, as of Dec. 31, the company had a staggering $625 billion order backlog from customers who were waiting for more infrastructure to come online.

However, one of the reasons Microsoft stock sold off over the past few months is that 45% of that backlog (or $281 billion) was attributable to ChatGPT creator OpenAI alone. In February, the startup announced some bad news: It will spend only $600 billion on computing capacity through 2030 across all providers=, reducing its previous forecast of $1.4 trillion. As a result, Microsoft’s order backlog might be overstated, which is something the company will probably clear up on April 29.

Nevertheless, demand for computing power would exceed supply for the foreseeable future even if we removed OpenAI from the picture entirely, so Azure likely delivered extremely fast growth yet again during the third quarter.

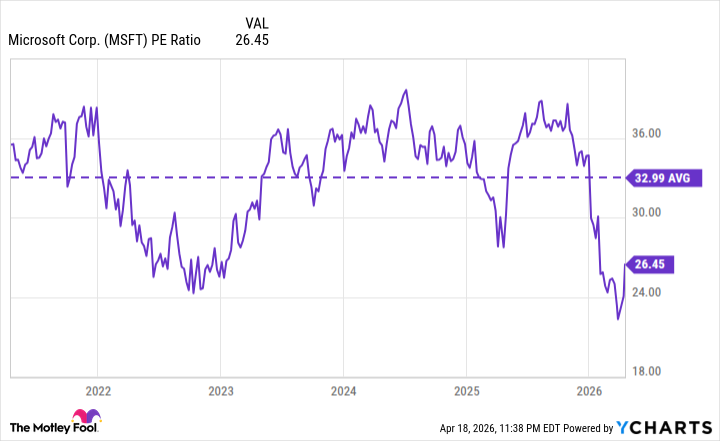

Microsoft’s valuation leaves plenty of room for upside

Based on Microsoft’s trailing-12-month earnings of $15.98 per share and its stock price of $422.79 at the market close on Friday, April 17, its price-to-earnings (P/E) ratio is just 26.4. That is a steep discount to its five-year average of 32.9, and it’s also lower than the P/E of the Nasdaq-100, which is currently 32.4.

MSFT PE Ratio data by YCharts

As a result, Microsoft stock looks undervalued right now, but I don’t think that will remain the case for long. If the company alleviates some of the uncertainty surrounding its cloud order backlog on April 29, while demonstrating strong Azure revenue growth and robust Copilot adoption, investors might feel more confident about buying its stock.

In terms of potential upside, the stock would have to climb by 24% just for its P/E ratio to trade in line with its five-year average of 32.9, so there could be strong returns on the table for investors who buy in ahead of the upcoming earnings report. However, it’s important to maintain a long-term view, because investors could reap much bigger rewards as Microsoft’s AI businesses mature over the next five years or so.