OpenAI launched its ChatGPT artificial intelligence (AI) application in November 2022, and it attracted over 100 million users in just two months. This marked the beginning of the AI boom, but some companies had been developing and even monetizing this revolutionary technology for several years prior.

Upstart Holdings (UPST +2.94%) has been using AI to assess the creditworthiness of potential borrowers since 2014. Today, the company’s algorithms might be even more predictive than traditional loan assessment tools, including Fair Isaac‘s FICO credit scoring system.

Upstart’s revenue exploded to a record high in 2025, and the company is expected to deliver another strong result in 2026. However, its stock has opened this year with a 40% decline, and it’s now trading at the cheapest level in almost three years. I think that spells opportunity for investors. Here’s why I predict the stock will double before 2026 is over.

Image source: Getty Images.

AI is transforming the lending business

The FICO credit scoring system takes into account just five core metrics to determine a borrower’s creditworthiness, including their existing debts and repayment history. Upstart’s algorithm measures over 2,500 data points to build a more complete profile of the borrower, which the company says can lead to a higher chance of approval with a more accurate interest rate.

It would take human loan assessors days or even weeks to analyze an equivalent amount of data, leading to an unsatisfactory customer experience. In the fourth quarter of 2025, Upstart’s algorithm handled 91% of all loan applications autonomously with no human intervention, which highlights the power of AI.

Upstart originated almost 1.5 million loans during 2025, a whopping 115% increase compared to 2024. Those loans had a total dollar value of $11 billion, which was up 86%. Simply put, the company’s AI-powered approach is clearly resonating with prospective borrowers.

Today’s Change

(2.94%) $0.80

Current Price

$28.06

Key Data Points

Market Cap

$2.8B

Day’s Range

$26.43 – $28.13

52wk Range

$23.96 – $87.30

Volume

27K

Avg Vol

5M

Gross Margin

97.62%

Unsecured personal loans make up the majority of Upstart’s originations, but the company is making a lot of headway in the automotive and home equity line of credit (HELOC) segments. In fact, originations grew fivefold in those two categories last year.

But this is only the beginning. Upstart chairman Dave Girouard believes AI will replace all human-led loan assessment methods within the next decade, leaving $25 trillion in global originations and $1 trillion in fee revenue up for grabs for companies just like this one.

Blistering revenue and earnings growth

Upstart earns fees for originating loans on behalf of banks and other financial institutions. It typically doesn’t lend any money itself, except for research and development purposes, but that might be about to change. Last month, the company announced it would apply for a national bank charter so it could accept deposits from consumers and use them to write loans. In other words, Upstart is preparing to launch America’s first AI-powered bank.

In 2025, Upstart generated a record $1.04 billion in revenue, which was a whopping 64% increase compared to 2024. It also generated $53.6 million in generally accepted accounting principles (GAAP) net income, which was a big swing from the $128.5 million net loss it delivered in the prior year.

After excluding one-off and noncash expenses like stock-based compensation, Upstart generated $230.4 million in adjusted earnings before interest, tax, depreciation, and amortization (EBITDA), which was a more than twentyfold increase compared to 2024.

According to estimates compiled by Yahoo! Finance, Wall Street analysts expect Upstart’s revenue and earnings to grow even further during 2026. However, if the company really does launch an AI-powered bank, its future financial results could eclipse anything it delivers this year.

Why Upstart stock could double by the end of 2026

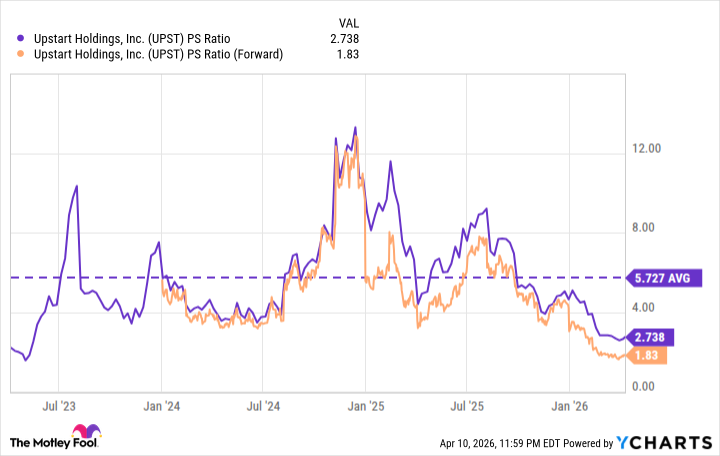

Upstart has a market capitalization of $2.5 billion as I write this, so based on the company’s 2025 revenue, its stock is trading at a price-to-sales (P/S) ratio of just 2.7. That is a hefty discount to its three-year average of 5.7, and it’s approaching the lowest point of the range over that period.

But based on Wall Street’s 2026 revenue estimate of $1.4 billion, Upstart stock is trading at an even more attractive forward P/S ratio of 1.8.

UPST PS Ratio data by YCharts

That suggests Upstart stock would have to climb by 50% before the end of 2026 just to maintain its current P/S ratio of 2.7. However, it would have to soar by 216% to bring its P/S ratio in line with its three-year average.

It might be a tall order to expect the stock to triple by the end of this year, but even if it delivers half that gain, it would still double from its current level. I think that could be a likely outcome because of Upstart’s strong revenue and earnings growth, but also because investors are likely to receive more bullish news in the coming quarters about the company’s plan to become a full-fledged AI bank.